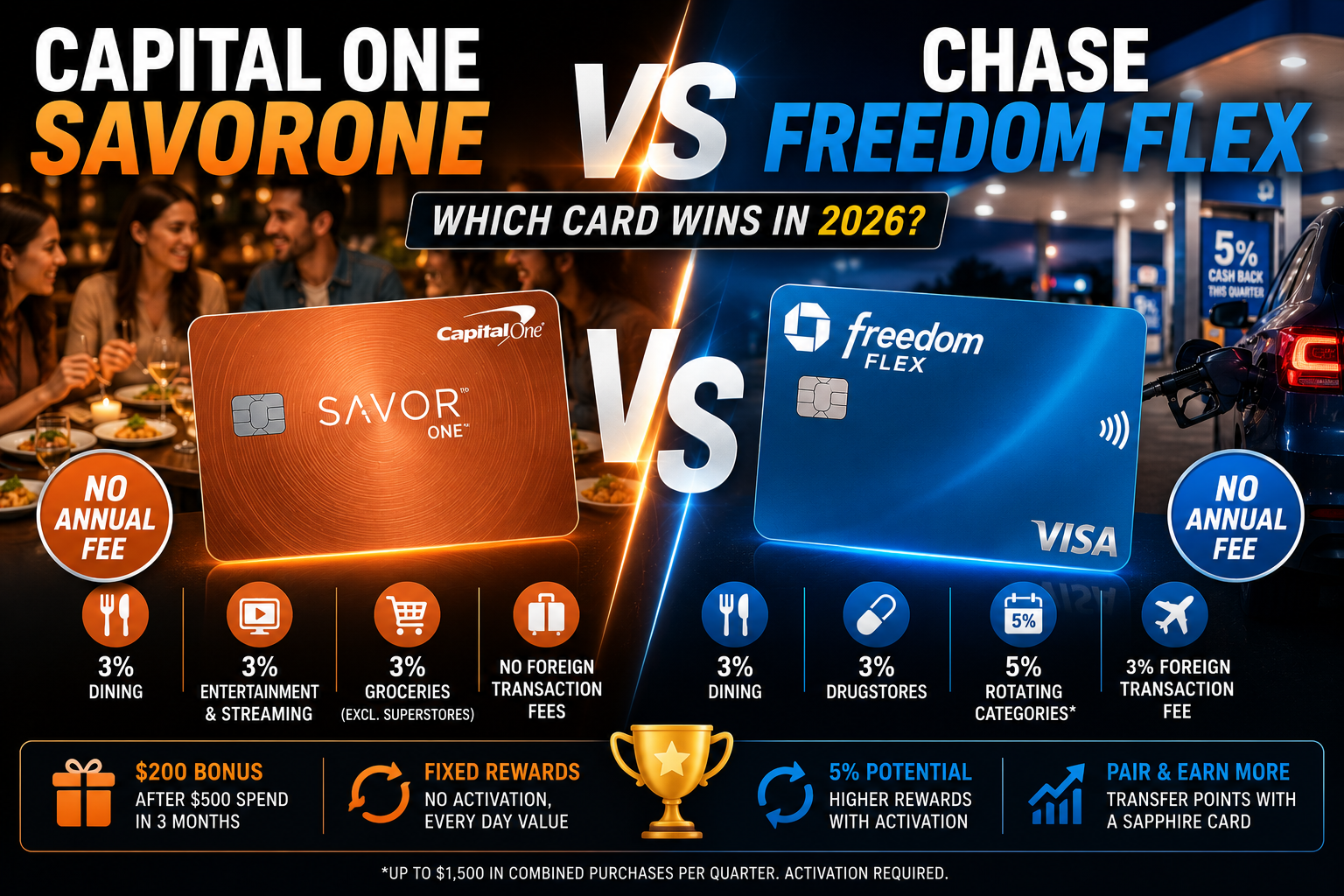

Capital One SavorOne vs Chase Freedom Flex 2026: Which Card Wins?

Both of these no-annual-fee cards reward dining heavily, but they get there in very different ways — one with fixed categories, the other with rotating ones. This Capital One SavorOne vs Chase Freedom Flex comparison breaks down the rewards structure, welcome bonuses, and perks so you can pick the right fit for how you actually spend.

Capital One SavorOne vs Chase Freedom Flex: Quick Comparison

| Feature | Capital One SavorOne | Chase Freedom Flex |

|---|---|---|

| Annual Fee | $0 | $0 |

| Dining & Entertainment | 3% dining, entertainment, streaming, groceries (excl. superstores) | 3% dining and drugstores (fixed, all year) |

| Rotating Categories | None | 5% on quarterly rotating categories (up to $1,500/quarter, must activate) |

| Travel Bonus | 5% hotels & rental cars via Capital One Travel | 5% via Chase Travel portal |

| Welcome Bonus | $200 after $500 spend in 3 months | $200 after $500 spend in 3 months |

| Foreign Transaction Fee | None | 3% |

| Points Transfer Partners | Yes, when paired with a Capital One miles card | Yes, when paired with a Chase Sapphire card |

In this Capital One SavorOne vs Chase Freedom Flex matchup, the biggest practical difference is effort: SavorOne’s categories are fixed year-round, while Freedom Flex requires activating new categories every quarter. For official terms, see Capital One’s official SavorOne page.

Where Each Card Wins

Capital One SavorOne wins for consistency and international travel. Its 3% dining, entertainment, streaming, and grocery categories never change or require activation, and it charges no foreign transaction fee — a real advantage over Freedom Flex’s 3% surcharge abroad.

Chase Freedom Flex wins for engaged optimizers. The 5% rotating categories (things like gas stations, Amazon, or PayPal in different quarters) can out-earn SavorOne’s fixed 3% if you’re willing to track and activate each quarter, and it fits naturally into a “Chase trifecta” with a Sapphire card for travel point transfers.

Pros and Cons

Capital One SavorOne Pros

- No foreign transaction fee, unlike Freedom Flex

- Fixed 3% categories, no quarterly activation needed

- 8% back on Capital One Entertainment purchases

- Simple, low-maintenance rewards structure

Chase Freedom Flex Pros

- 5% rotating categories can beat SavorOne’s flat 3% in the right quarters

- Pairs into the Chase Ultimate Rewards ecosystem with a Sapphire card

- Broader redemption options through Chase Travel

Who Should Get Each Card

| Your Situation | Best Card |

|---|---|

| You travel internationally often | ✅ Capital One SavorOne |

| You don’t want to track rotating categories | ✅ Capital One SavorOne |

| You already hold a Chase Sapphire card | ✅ Chase Freedom Flex |

| You spend heavily on streaming and groceries | ✅ Capital One SavorOne |

| You’re comfortable activating categories quarterly for higher rates | ✅ Chase Freedom Flex |

Looking for more dining-focused options? Check our Best Credit Card for Dining guide, or see how a flat-rate alternative compares in our Citi Double Cash vs Chase Freedom Unlimited review.

Frequently Asked Questions

Does Capital One SavorOne charge foreign transaction fees?

No, SavorOne has no foreign transaction fee, while Chase Freedom Flex charges 3% on purchases made abroad.

Do I need to activate categories with Capital One SavorOne?

No, SavorOne’s 3% categories (dining, entertainment, streaming, and groceries) are fixed year-round with no activation required, unlike Freedom Flex’s rotating 5% categories.

Can Chase Freedom Flex rewards transfer to travel partners?

Only if you also hold a premium Chase card like the Sapphire Preferred or Sapphire Reserve; on its own, Freedom Flex earns straight cash back.

Which card has a better welcome bonus?

Both currently require a similar $500 spend in 3 months for a comparable $200 bonus, so the welcome offers are roughly equivalent.

Can I hold both cards at the same time?

Yes, since they’re issued by different banks with separate approval rules, and pairing them can help maximize rewards across more spending categories.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Card terms, fees, and rewards are subject to change by the issuer; always verify current rates and fees directly with Capital One or Chase before applying. We may earn a commission from partner links, which does not affect the objectivity of our reviews.